SPONSORED

Market Watch: July 26

Jul 29, 2024 | 11:13 AM

-

Share on Facebook

-

Share on Twitter

- Copy Link

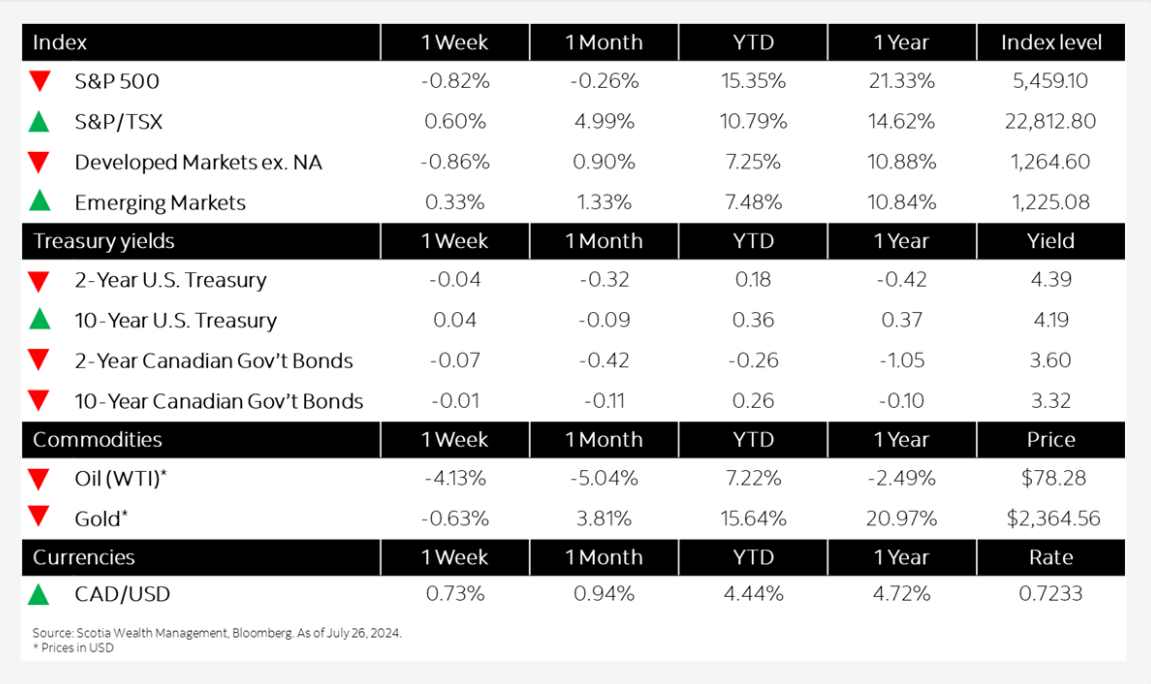

This week’s highlights

- Megacap tech and chip stocks continue to weigh on equity markets

- Bond yields mixed following release of Fed’s preferred inflation gauge

- Bank of Canada cuts key rate to 4.5%, tees up additional easing

- U.S. economic growth regains momentum in second quarter as inflation slows

- Eurozone PMI composite hits 5-month low

- In the news: Chip stocks face setback despite strong demand

Week in review

Megacap tech and chip stocks continue to weigh on equity markets