sponsored

Market Watch: July 5, 2024

Jul 6, 2024 | 10:45 AM

-

Share on Facebook

-

Share on Twitter

- Copy Link

This week’s highlights

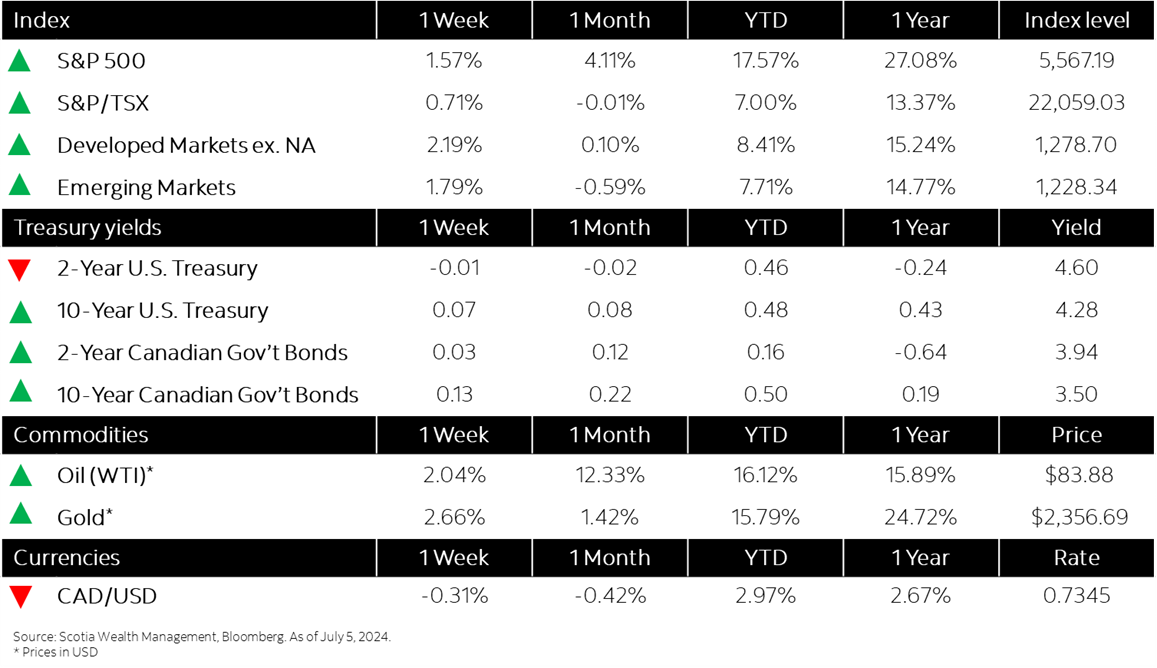

- U.S., Canadian markets steadily advance amid short trading week

- Bond yields mixed as investors bet on two Fed rate cuts following June jobs data

- Canadian unemployment rate continues to climb

- U.S. jobs report shows unemployment ticked up to 4.1%

- Eurozone manufacturing sector faces accelerated downturn in June

- In the news: Volkswagen, Rivian agree to technology joint venture