Sponsored

Market Watch: June 21

Jun 24, 2024 | 2:54 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- U.S. markets edge higher as tech stocks take centre stage

- Global yields assess data indicating a slowing economy

- Annual pace of Canadian housing starts in May up 10% from April

- U.S. retail sales miss expectations in May as lower prices for gasoline, motor vehicles weigh

- Bank of England holds off on rate cut despite easing inflation

- In the news: Boeing’s horrible, no good, very bad year

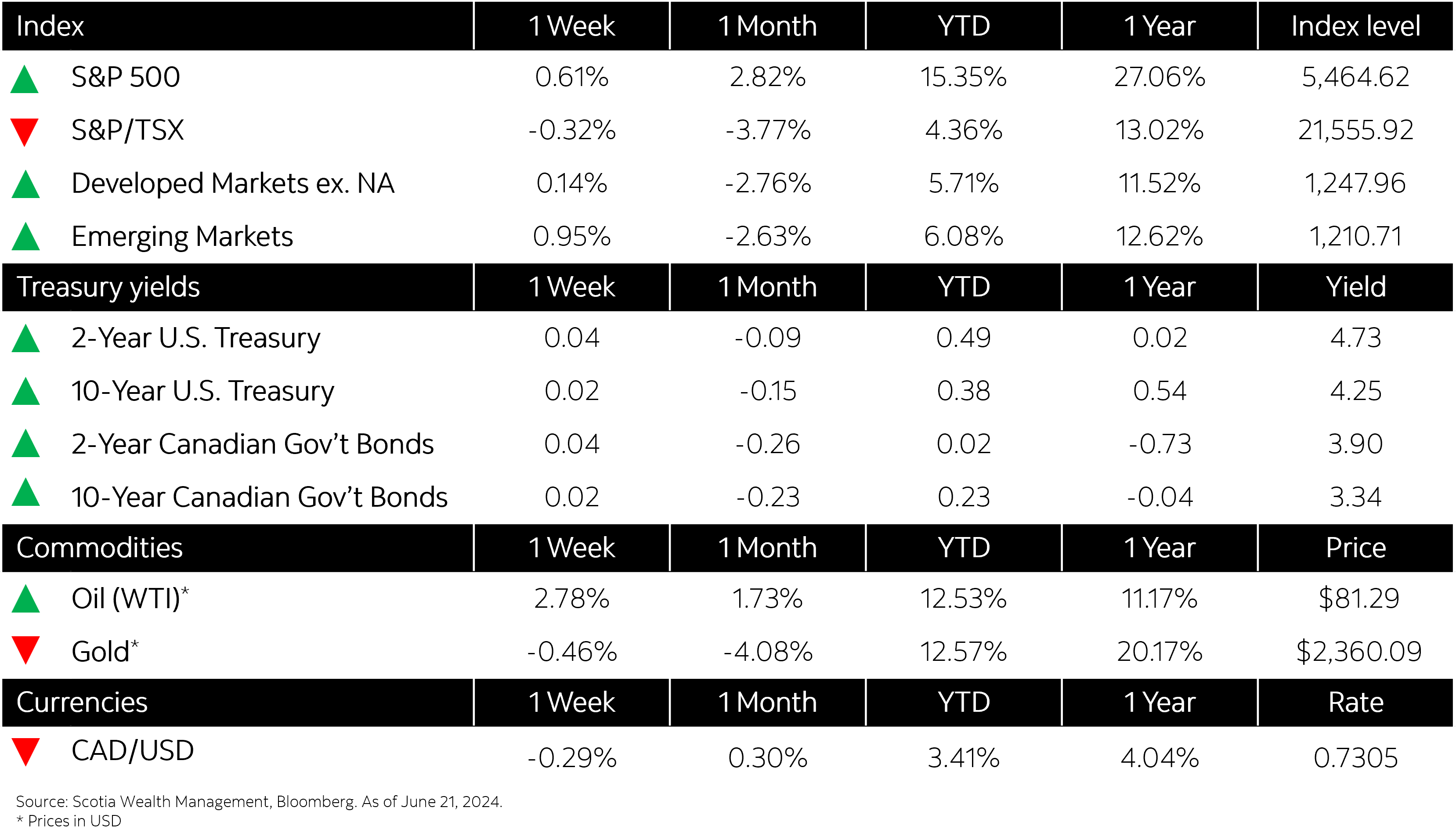

Week in review

U.S. markets edge higher as tech stocks take centre stage