Sponsored

Market Watch: May 31

Jun 3, 2024 | 11:40 AM

-

Share on Facebook

-

Share on Twitter

- Copy Link

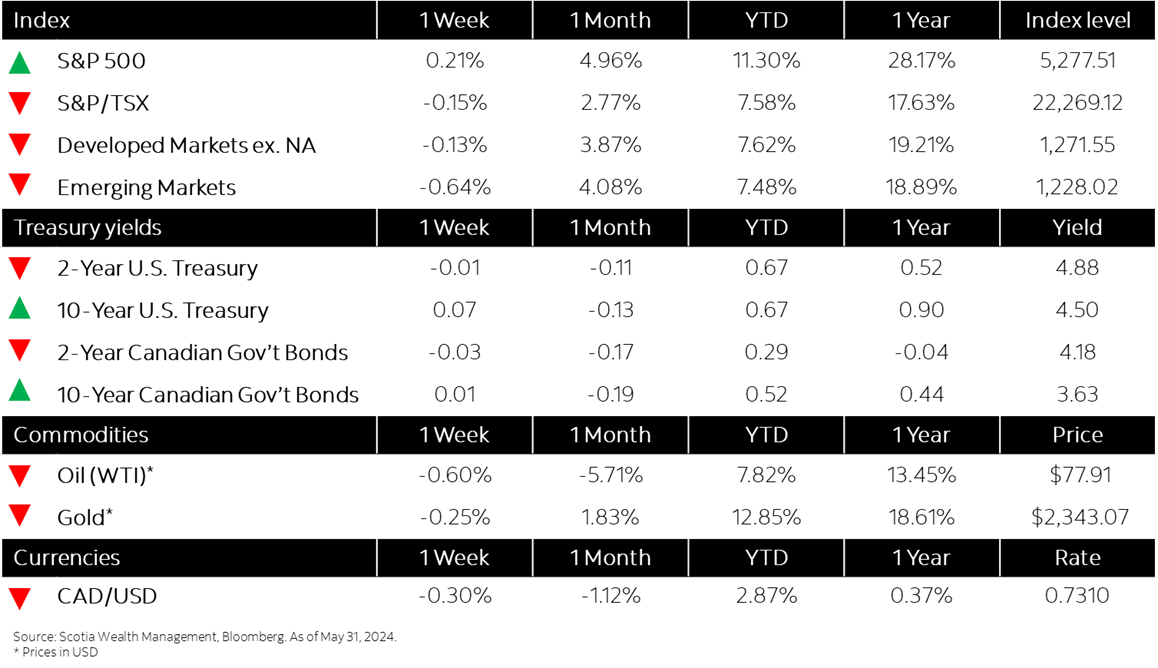

This week’s highlights

- Equity markets give up some gains despite steady U.S. inflation

- Sovereign bonds move higher following U.S. PCE reading

- Canadian economy misses first-quarter growth forecast; April GDP likely up 0.3%

- U.S. economic growth revised lower for first quarter

- IMF raises China economic growth forecasts

- In the news: Major energy companies forge strategic alliances through consolidation

Week in review

Equity markets give up some gains despite steady U.S. inflation