Sponsored

Market Watch: May 24

May 27, 2024 | 2:00 PM

-

Share on Facebook

-

Share on Twitter

- Copy Link

This week’s highlights

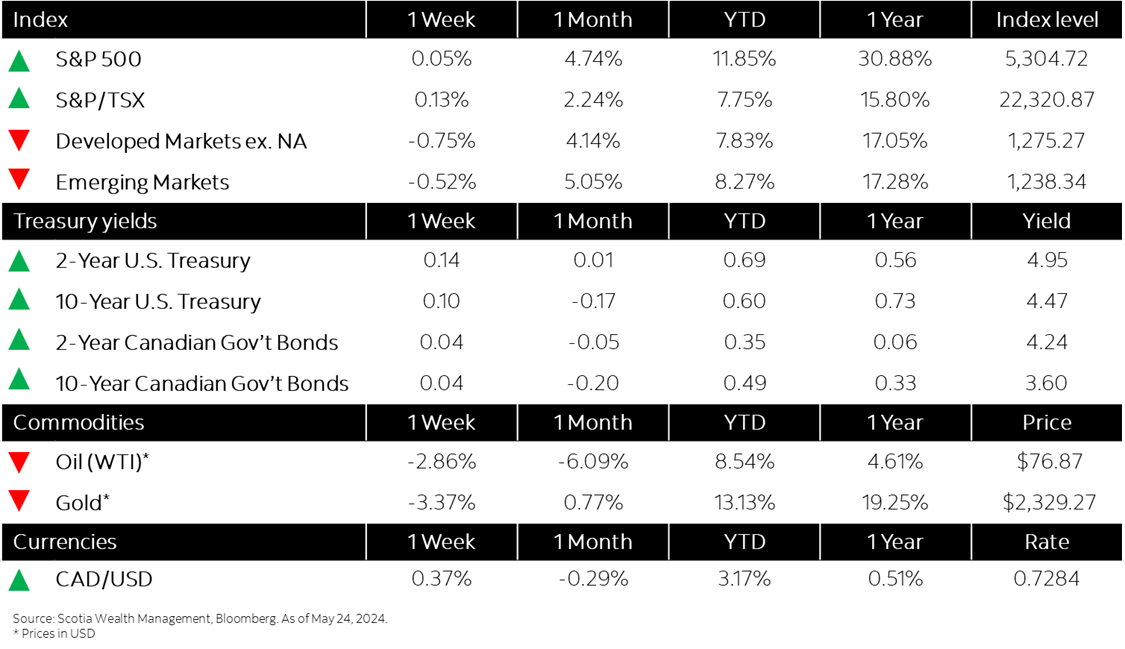

- North American markets close higher despite late-week correction

- Economic acceleration pushes bonds to give up recent gains

- Inflation in Canada cools to 2.7% in April, increasing odds of a summer interest rate cut

- U.S. home sales fall again in April after high mortgage rates dampen activity

- China benchmark lending rates held steady

- In the news: Anglo American, BHP extend talks following third rejected bid

Week in review

North American markets close higher despite late-week correction