Sponsored

Market Watch: April 26

Apr 29, 2024 | 10:48 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

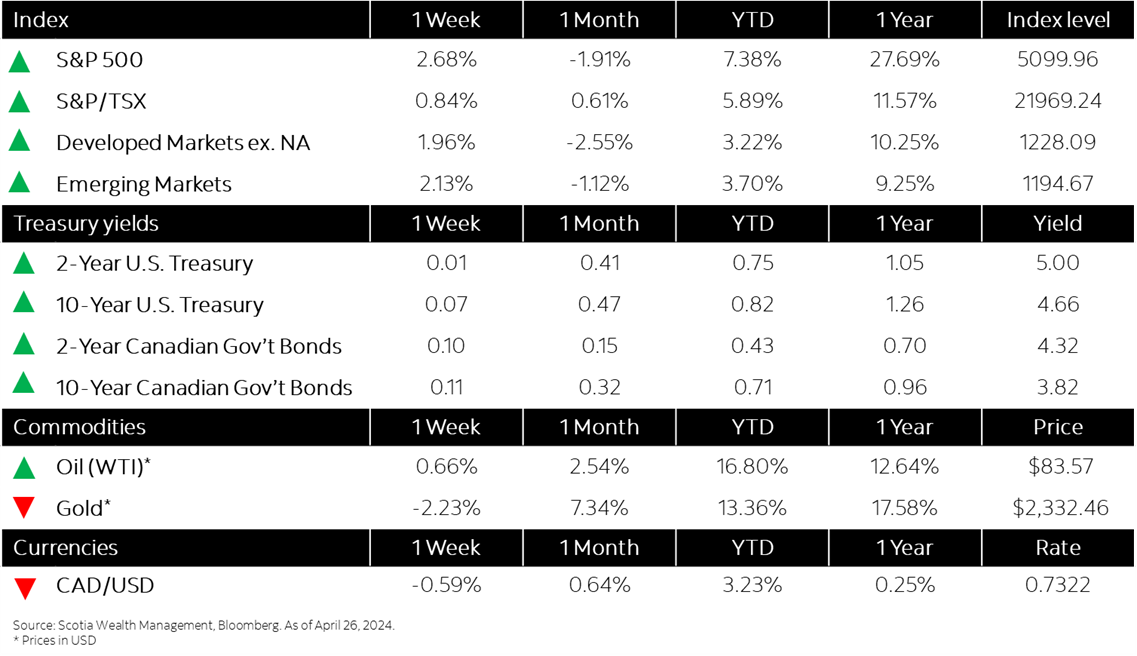

This week’s highlights

- Equity markets make about face following strong earnings reports

- Yields broadly higher following GDP reading and Fed’s preferred inflation measure

- Canadian retail sales slip 0.1% in February, seen flat in March

- U.S. economic growth slows to 1.6%

- German business sentiment continues to brighten

- In the news: Waning sales of EVs not enough to dissuade investment from manufacturers

Week in review

Equity markets make about face following strong earnings reports