Sponsored

Market Watch: January 26

Jan 29, 2024 | 4:04 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

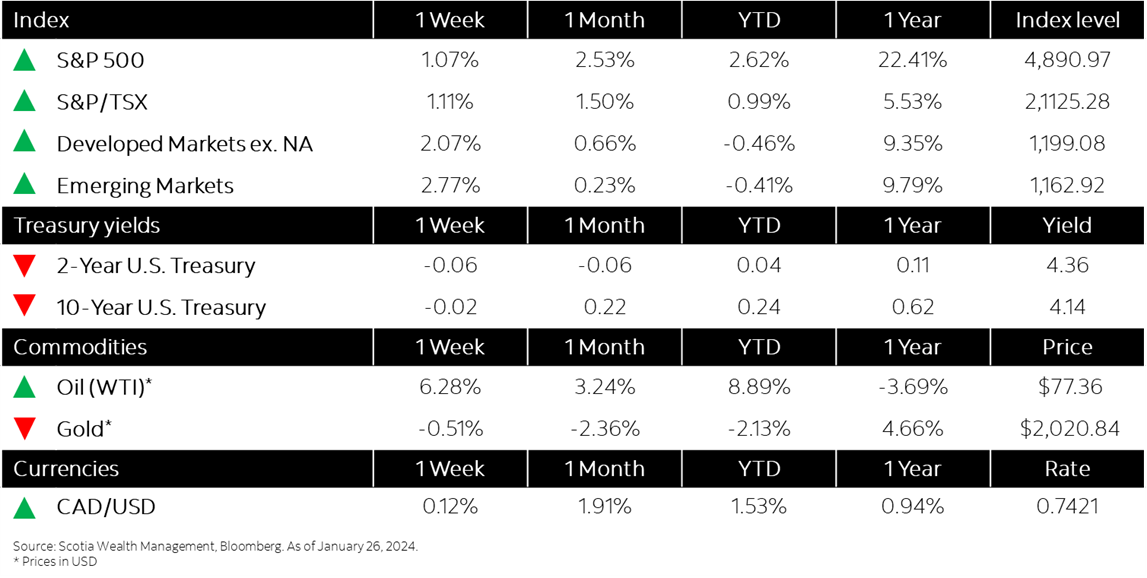

This week’s highlights

- Global equities advance cautiously on growth and inflation data

- Fixed income markets rally on inflation data and rate cut hopes

- Bank of Canada keeps key interest rate at 5%

- U.S. economy grew 3.1% over the past year

- China moves to boost bank lending in broad effort to prop up growth

- Concerns arise over potential supply chain shock in wake of Red Sea attacks

Week in review

Global equities advance cautiously on growth and inflation data